Strategy April 08, 2021

From Startup to Sensation: How to Land a Unicorn Client

Distributors reveal how they’ve met the growing needs of small companies that exploded into major corporations.

How do you catch a unicorn?

Tom Economou knows. After all, Sunrise Identity Powered by HALO (asi/356000) has been working with Starbucks for 20 years.

It all started with one connection in the coffee company’s (at the time) small marketing department. A pitch was made, but Starbucks already had a promotional products distributor. Undeterred, a now-retired account executive with Sunrise thanked the marketing person for her time and reiterated that Sunrise would be there if the other distributor ever failed to meet Starbucks’ needs.

“That weekend, the marketing contact was shopping at a local market and found a bunch of off-brand Starbucks merchandise being sold by her current supplier,” says Economou, senior vice president of sales at Sunrise. “She fired them on the spot and called us on Monday.”

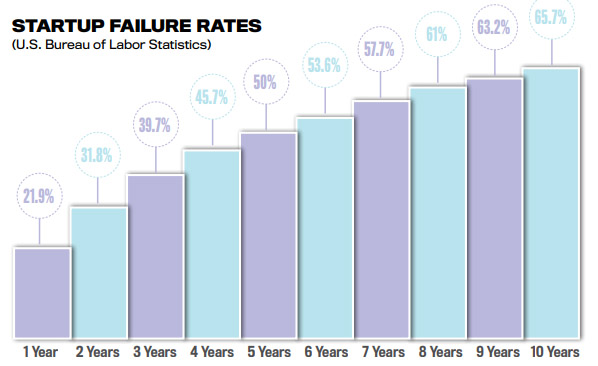

Don't Miss: How to Know When a Startup Won’t Last

Starbucks was already a burgeoning brand at the time, but Economou admits that nobody on staff expected it would balloon to over 340,000 employees worldwide. He quickly realized Sunrise would have to keep up with the growing demands or risk being replaced. As a result, the two companies cultivated a strong, mutually beneficial partnership: Sunrise created Starbucks’ first employee online store, which it still manages today, and Starbucks helped Sunrise develop its factory compliance and product safety program.

“We could see the energy and purpose behind their work,” Economou says. “Starbucks made us a better company.”

Every distributor wants the best for their clients, especially those they’ve been with since the beginning. Their success is your success – the bigger they get, the more opportunities you can capitalize on.

But targeting a young company is risky. In 2019, startup failure rates were around 90%, according to the Small Business Administration (SBA). (That percentage most likely rose in 2020 due to the COVID-19 pandemic.) The U.S. Bureau of Labor Statistics reports that 22% of startups fail in the first year, 32% shut down in the second year and 50% cease operations in the fifth year. Most cited reasons for startup failure are lack of financing, lack of research, dissolved partnerships, too much competition and ineffective marketing.

And unicorns? The term, coined by venture capitalist Aileen Lee, refers to a privately held startup with a value of over $1 billion. They’re exceedingly rare – hence the name. Crunchbase reported last year that there were 600 such companies.

Partnering with a startup is similar to investing, says Ronnie Teja, founder and CEO of Branzio Watches, a 2015 startup that now does $18 million in revenue. “Before you invest in any business, you must ask yourself three questions: What problem is being solved? Can you define the target market? Is the business scalable?” says Teja. “If you can answer those questions, you can invest your time, money and resources in the business.”

Of course, it takes two to tango. Finding a unicorn isn’t only about the startup’s potential, but your belief in their success, too. “If you partner with a startup that you don’t believe has extreme potential for growth, you’re likely not going to end up helping them on their journey,” says Peter Horne, content lead at Geoff McDonald and Associates. “When we believe in something, we tend to try harder to make it succeed. For a startup to be successful, all moving parts, including you, need to believe in that success and should be working toward the same goal.”

Lightning in a Bottle

It’s easier for distributors to find a unicorn than it is to catch one.

There are several online platforms to search for startups, such as AngelList, Wefunder and Gust. You could also attend pitch nights, where startups present their product or service to a large audience of entrepreneurs and investors. The goal is to raise money, recruit talent and seek help to grow their company.

“You’re wearing 100 different hats as a startup, and usually the hardest part of the equation is marketing and customer acquisition,” says Shane Neman, business expert and venture capitalist who specializes in startups in the technology, hospitality and real estate industries. “Most startup founders are tech guys or inventors who only know how to build an awesome product. They’d love to be able to give the marketing responsibility to someone they can trust.”

“We’ve worked so closely with Shopify that I feel like I’m part of their team.” Stephen Musgrave, Rightsleeve

Getting involved with incubators and accelerators is another entry point into the startup market. An incubator is a collaborative program designed to help startups in their infancy succeed by providing workspace, seed funding, mentoring and training. An accelerator is similar, but only lasts a few months and is more of a business boot camp.

“Startups usually consist of young enthusiasts that want to change the world and make it a better place,” says Emma Sargsyan, founder and CEO of Saege Consultants, a public relations, event management and digital media services agency. “In my experience, any startup needs motivation and support from a mentor. Proper management and motivation will nurture the startup and make it a well-established, self-reliant firm.”

Startups that are about to explode with growth typically have tangible, telltale signs, says Baron Christopher Hanson, owner and lead consultant of RedBaronUSA and a business expert who’s written for the Harvard Business Review. These include considerable evidence of expansion, such as real estate or architectural transactions, merger and acquisition activity or high-profile industry professionals being hired left and right.

“By contrast, wannabe startups that are all talk and no action typically have little or nothing tangible to be invested in,” Hanson says. “The sales pitch may go on and on, and there might be lots of social media chatter, yet actual evidence of growth or cascading revenues or a big news story are nowhere to be found.”

As with any potential client, it’s important to establish yourself first. Referrals and word of mouth remain the best advertising, so taking care of your current clients is even more important. You also need to promote your products, services and accomplishments on social media, maintaining an active presence and engaging with your followers. You never know when a potential client, especially a startup, may be looking at your profile and considering whether you’d make a good partner.

“In your spare time, you need to be networking,” says Matt Lerner, founder and managing partner at Torchlight Consulting, which works with founders of early-stage companies. “Don’t just focus on finding potential prospects and partners. You need to be an evangelist for your company and a leader in your field.”

Thanks to an effective email marketing campaign and social media strategy, Garland, TX-based Bob Lilly Promo (asi/254138) found a unicorn at its front door.

Founded in 2012, Arctic Wolf Networks (AWN) is a “security operations center-as-a-service” provider, supplying customers with the staff and technology they need to manage their cybersecurity. The Silicon Valley company approached Bob Lilly in 2019 to create its online store and manage its warehouse inventory. This past October, Arctic Wolf secured $200 million in Series E funding at a valuation of $1.3 billion. To celebrate, Bob Lilly sent a kit containing a custom award, plush toy, engraved pint glass and leather coaster to over 700 Arctic Wolf employees.

“Be prepared to fulfill orders both large and small, and to roll with the joys and pains associated with any startup relationship.” Baron Christopher Hanson, RedBaronUSA

“We’ve been meeting their needs just fine,” says Jennifer Schuller, senior account manager at Bob Lilly. “We’ve had to pivot because of the pandemic to do way more drop-shipments and mailings, but you have to be ready to handle the volume as it comes. I haven’t treated them any differently because we’ve always treated them as a top priority.”

The secret to meeting the needs of any blossoming startup, Hanson says, is to develop a system that can expand or retract based on the actual demand for your product or service. “Your plan should be designed and priced for if things go well or if they slow down a bit,” Hanson says. “Be prepared to fulfill orders both large and small, and to roll with the joys and pains associated with any startup relationship.”

Personal Touch

Toronto-based Rightsleeve (asi/308922) almost let a unicorn slip through its fingers.

On a Friday afternoon in 2012, the Canadian distributor was asked for a quote on an order of 1,000 sweatshirts. The person who usually handled such requests was off that week, and by the time someone finally responded, the potential customer had moved on. Stephen Musgrave, an account manager at the time, followed up by sending a self-promo, thanking them for reaching out and hoping to work together in the future.

The potential customer liked the gift so much they tweeted about it. A few weeks later, Musgrave had lunch with representatives of his new client, which has become Rightsleeve’s largest client: Shopify.

“I don’t let anybody around here forget it,” laughs Musgrave, now the vice president and general manager of Rightsleeve. “Those little touches of customer experience can really change how a relationship works.”

Over the past decade, Rightsleeve has concentrated on the startup community for several reasons. First, it’s easier to communicate with decision-makers because there’s less red tape. Secondly, startups have more potential for growth compared to most small businesses because they’re built to scale. Most importantly, startups truly value branded merchandise, especially T-shirts and hoodies.

“It’s a powerful moment when you understand their business and speak their language,” Musgrave says. “We can be more helpful because they have fewer resources to do things.”

Failure to Launch: Two-thirds of startups won’t last 10 years, which makes it important to be an early brand steward for these businesses to help them grow into a runaway success and lead to major future promo sales.

As with any client, though, becoming a startup’s full-service provider doesn’t happen overnight. Musgrave says it took two years of handling spontaneous piecemeal orders before earning Shopify’s consistent business. The turning point in their relationship was when Rightsleeve took over the e-commerce platform’s employee onboarding kits. “Startups tend to make people wear a lot of hats,” Musgrave says. “In addition to her regular job, this woman was tasked with buying swag, packing it up and giving it out. We talked about the process and how much of a pain it was because they were hiring five people every week.”

In 2014, $3.8 billion in gross merchandise volume passed through Shopify sites and the company generated $105 million in revenue, The Motley Fool reported. One year later, Shopify went public. The company priced its IPO at $17 per share, above the initially proposed range of $14-$16. Rightsleeve worked on projects for Shopify’s employees prior to the IPO, including some special gifts for the senior management team. The distributor also made labels out of the company banner that was hung on the New York Stock Exchange.

“The IPO was a big deal for us,” Musgrave says. “We’ve worked so closely with them that I feel like I’m part of their team.”

As Shopify’s merchants swelled from 162,000 to more than a million, Musgraves admits it was challenging to meet the growing needs. Long-term warehouse fulfillment was a foreign concept to the distributor, but it was an essential part in servicing the juggernaut. Fortunately, Rightsleeve was acquired by Top 40 distributor Genumark (asi/204588), which provided much larger warehousing capabilities. “Anybody who builds a really large client relationship and doesn’t worry about it is crazy,” Musgrave says. “Now we feel a little more at peace as we focus on growing the relationship even more.”

2020 was a record year for Shopify, as online shopping soared during the COVID-19 pandemic. The company reported total revenue of $2.9 billion, an 86% increase over 2019. The holiday season provided a significant boost with Q4 revenue of $977.7 million, a 94% increase from Q4 2019. As the company increases investment in the Shopify Fulfillment Network, international expansion and innovative products like Shop App, Rightsleeve is ready to come along for the ride.

“A big part of this relationship was us learning and growing along with them,” Musgrave says. “If you’re working with a startup that has already ramped up and you don’t know what to do, travel back in time and teach yourself new stuff. You have to keep evolving with your client.”

John Corrigan is a senior writer for ASI Media. Since joining ASI in 2016, he has produced the award-winning PromoGram newsletter and won an ASBPE award in 2020 for Best Profile. Tweet: @JCorr_ASI; email: jcorrigan@asicentral.com